Gold ORB Strategy (15-min Range, 5-min Entry)The Gold ORB (Opening Range Breakout) Strategy is designed for day traders looking to capitalize on the price action in the early part of the trading day, specifically using a 15-minute range for identifying the opening range and a 5-minute timeframe for breakout entries. The strategy trades the Gold market (XAU/USD) during the New York session.

Opening Range: The strategy defines the Opening Range (ORB) between 9:30 AM EST and 9:45 AM EST using the highest and lowest points during this 15-minute window.

Breakout Entries: The strategy enters trades when the price breaks above the ORB high for a long position or below the ORB low for a short position. It waits for a 5-minute candle close outside the range before entering a trade.

Stop Loss and Take Profit: The stop loss is placed at 50% of the ORB range, and the take profit is set at twice the ORB range (1:2 risk-reward ratio).

Time Window: The strategy only executes trades before 12:00 PM EST, avoiding late-day market fluctuations and consolidations.

Cari dalam skrip untuk "take profit"

Cyclical CALL/PUT StrategyThis script identifies optimal CALL (long) and PUT (short) entries using a cyclical price wave modeled from a sine function and confirmed with trend direction via a 200 EMA.

Strategy Highlights:

Cycle-Based Signal: Detects market rhythm with a smoothed sinusoidal wave.

Trend Confirmation: Filters entries using a customizable EMA (default: 200).

Auto-Scaling: Wave height adjusts dynamically to price action volatility.

Risk Parameters:

Take Profit: Default 5% (customizable)

Stop Loss: Default 2% (customizable)

Signal Triggers:

CALL Entry: Price crosses above the scaled wave and in an uptrend

PUT Entry: Price crosses below the scaled wave and in a downtrend

Inputs:

Cycle Length

Smoothing

Wave Height

EMA Trend Length

Take Profit %

Stop Loss %

Visuals:

Gray line = Scaled Cycle Wave

Orange line = 200 EMA Trend Filter

Best For: Traders looking to make 1–2 high-probability trades per week on SPY or other highly liquid assets.

Timeframes: Works well on 2-min, 15-min, and daily charts.

DEMA Trend Oscillator Strategy📌 Overview

The DEMA Trend Oscillator Strategy is a dynamic trend-following approach based on the Normalized DEMA Oscillator SD.

It adapts in real-time to market volatility with the goal of improving entry accuracy and optimizing risk management.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main goal of this strategy is to respond quickly to sudden price movements and trend reversals,

by combining momentum-based signals with volatility filters.

It is designed to be user-friendly for traders of all experience levels.

✨ Key Features

Normalized DEMA Oscillator: A momentum indicator that normalizes DEMA values on a 0–100 scale, allowing intuitive identification of trend strength

Two-Bar Confirmation Filter: Requires two consecutive bullish or bearish candles to reduce noise and enhance entry reliability

ATR x2 Trailing Stop: In addition to fixed stop-loss levels, a trailing stop based on 2× ATR is used to maximize profits during strong trends

📊 Trading Rules

Long Entry:

Normalized DEMA > 55 (strong upward momentum)

Candle low is above the upper SD band

Two consecutive bullish candles appear

Short Entry:

Normalized DEMA < 45 (downward momentum)

Candle high is below the lower SD band

Two consecutive bearish candles appear

Exit Conditions:

Take-profit at a risk-reward ratio of 1.5

Stop-loss triggered if price breaks below (long) or above (short) the SD band

Trailing stop activated based on 2× ATR to secure and extend profits

💰 Risk Management Parameters

Symbol & Timeframe: Any (AUDUSD 5M example)

Account size (virtual): $3000

Commission: 0.4PIPS(0.0004)

Slippage: 2 pips

Risk per trade: 5%

Number of trades (backtest):534

All parameters can be adjusted based on broker specifications and individual trading profiles.

⚙️ Trading Parameters & Considerations

Indicator: Normalized DEMA Oscillator SD

Parameter settings:

DEMA Period (len_dema): 40

Base Length: 20

Long Threshold: 55

Short Threshold: 45

Risk-Reward Ratio: 1.5

ATR Multiplier for Trailing Stop: 2.0

🖼 Visual Support

The chart displays the following visual elements:

Upper and lower SD bands (±2 standard deviations)

Entry signals shown as directional arrows

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by “Normalized DEMA Oscillator SD” by QuantEdgeB,

but introduces enhancements such as a two-bar confirmation filter and an ATR-based trailing stop.

Compared to conventional trend-following strategies, it offers superior noise filtering and profit optimization.

✅ Summary

The DEMA Trend Oscillator Strategy is a responsive and practical trend-following method

that combines momentum detection with adaptive risk management.

Its visual clarity and logical structure make it a powerful and repeatable tool

for traders seeking consistent performance in trending markets.

⚠️ Always apply appropriate risk management. This strategy is based on historical data and does not guarantee future results.

Phantom Trigger Phantom Trigger – Precision Trend Execution with TP1/TP2 and Weak Trend Exits

Phantom Trigger is a professional-grade trend-following strategy designed for crypto and high-volatility assets. It combines advanced trend detection with precise risk-managed exits using a multi-level take-profit system.

🔍 What It Does

Identifies strong directional moves using a multi-stage smoothed trend model

Confirms entries using structure-based logic and volume pressure

Filters trades using bias zones, confirmation levels, and trend acceleration

Automatically manages trades with two-stage take-profits (TP1 and TP2)

Exits early on trend weakness before reversal

Includes a styled real-time dashboard and bar coloring for visual guidance

Sends bot-compatible alerts for multi-exchange automation

⚙️ Core Components

Trend Engine: A smoothed dynamic filter detects real-time trend direction and momentum shifts

Bias Structure: Mid-high/low range-based logic determines if price is favoring bullish or bearish structure

Confirmation Levels: Short- and long-term zone crossovers confirm directional alignment

Volume Filter: Detects volume expansion spikes to validate strong breakout potential

TP1/TP2 Logic: Dynamically sets two profit targets and executes partial and full exits automatically

Weak Trend Exit: Closes positions one bar before reversal using directional filters

🧠 How to Use

Works best on crypto (1H, 4H) and high-volume instruments

Use dashboard stats to monitor position status, PnL, and TP1/TP2 progression

Alerts are pre-labeled and compatible with bots like 3Commas, Wunderbit, etc.

Can be adapted for both scalping and swing trading

📊 Dashboard

The built-in real-time dashboard displays current trade status, entry price, TP1/TP2 progress, win rate, profit factor, and bars since entry. It updates live with every candle and provides a quick-glance overview to support your decision-making during active trades.

🧠 How to Use

Works best on crypto (1H, 4H) and high-volume instruments

Use dashboard stats to monitor position status, PnL, and TP1/TP2 progression

Alerts are pre-labeled and compatible with bots like 3Commas, Wunderbit, etc.

Can be adapted for both scalping and swing trading

⚠️ Disclaimer

This script is for educational purposes only and does not constitute financial advice. Always test strategies thoroughly using demo or backtesting environments before applying to live markets. Past performance is not indicative of future results.

TrendTwisterV1.5 (Forex Ready + Indicators)A Precision Trend-Following TradingView Strategy for Forex**

HullShiftFX is a Pine Script strategy for TradingView that combines the power of the **Hull Moving Average (HMA)** and a **shifted Exponential Moving Average (EMA)** with multi-layered momentum filters including **RSI** and **dual Stochastic Oscillators**.

It’s designed for traders looking to catch high-probability breakouts with tight risk management and visual clarity.

Chart settings:

1. Select "Auto - Fits data to screen"

2. Please Select "Scale Price Chart Only" (To make the chart not squished)

### ✅ Entry Conditions

**Long Position:**

- Price closes above the 12-period Hull Moving Average.

- Price closes above the 5-period EMA shifted forward by 2 bars.

- RSI is above 50.

- Stochastic Oscillator (12,3,3) %K is above 50.

- Stochastic Oscillator (5,3,3) %K is above 50.

- Hull MA crosses above the shifted EMA.

**Short Position:**

- Price closes below the 12-period Hull Moving Average.

- Price closes below the 5-period EMA shifted forward by 2 bars.

- RSI is below 50.

- Stochastic Oscillator (12,3,3) %K is below 50.

- Stochastic Oscillator (5,3,3) %K is below 50.

- Hull MA crosses below the shifted EMA.

---

## 📉 Risk Management

- **Stop Loss:** Set at the low (for long) or high (for short) of the previous 2 candles.

- **Take Profit:** Calculated at a risk/reward ratio of **1.65x** the stop loss distance.

---

## 📊 Indicators Used

- **Hull Moving Average (12)**

- **Exponential Moving Average (5) **

- **Relative Strength Index (14)**

- **Stochastic Oscillators:**

- %K (12,3,3)

- %K (5,3,3)

Dkoderweb repainting issue fix strategyHarmonic Pattern Recognition Trading Strategy

This TradingView strategy called "Dkoderweb repainting issue fix strategy" is designed to identify and trade harmonic price patterns with optimized entry and exit points using Fibonacci levels. The strategy implements various popular harmonic patterns including Bat, Butterfly, Gartley, Crab, Shark, ABCD, and their anti-patterns.

Key Features

Pattern Recognition: Identifies 17+ harmonic price patterns including standard and anti-patterns

Fibonacci-Based Entries and Exits: Uses customizable Fibonacci levels for precision entries, take profits, and stop losses

Alternative Timeframe Analysis: Option to use higher timeframes for pattern identification

Heiken Ashi Support: Optional use of Heiken Ashi candles instead of regular candlesticks

Visual Indicators:

Pattern visualization with ZigZag indicator

Buy/sell signal markers

Color-coded background to highlight active trade zones

Customizable Fibonacci level display

How It Works

The strategy uses a ZigZag-based pattern identification system to detect pivot points

When a valid harmonic pattern forms, the strategy calculates the optimal entry window using the specified Fibonacci level (default 0.382)

Entries trigger when price returns to the entry window after pattern completion

Take profit and stop loss levels are automatically set based on customizable Fibonacci ratios

Visual alerts notify you of entries and exits

The strategy tracks active trades and displays them with background color highlights

Customizable Settings

Trade size

Entry window Fibonacci level (default 0.382)

Take profit Fibonacci level (default 0.618)

Stop loss Fibonacci level (default -0.618)

Alert messages for entries and exits

Display options for specific Fibonacci levels

Alternative timeframe selection

This strategy is designed to fix repainting issues that are common in harmonic pattern strategies, ensuring more reliable signals and backtesting results.

NY First Candle Break and RetestStrategy Overview

Session and Time Parameters:

The strategy focuses on the New York trading session, starting at 9:30 AM and lasting for a predefined session length, typically 3 to 4 hours. This timing captures the most active market hours, providing ample trading opportunities.

Strategy Parameters:

Utilizes the Average True Range (ATR) to set dynamic stop-loss levels, ensuring risk is managed according to market volatility.

Employs a reward-to-risk ratio to determine take profit levels, aiming for a balanced approach between potential gains and losses.

Strategy Settings:

Incorporates simple moving averages (EMA) and the Volume Weighted Average Price (VWAP) to identify trend direction and price levels.

Volume confirmation is used to validate breakouts, ensuring trades are based on significant market activity.

Trade Management:

Features a trailing stop mechanism to lock in profits as the trade moves in favor, with multiple take profit levels to secure gains incrementally.

The strategy is designed to handle both long and short positions, adapting to market conditions.

Alert Settings:

Provides alerts for key events such as session start, breakout, retest, and entry signals, helping traders stay informed and act promptly.

Visual cues on the chart highlight entry and exit points, making it easier for beginners to follow the strategy.

This strategy is particularly suited for the current volatile market environment, where simplicity and clear guidelines can help beginner traders navigate the complexities of trading. It emphasizes risk management and uses straightforward indicators to make informed trading decisions.

I put together this Trading View scalping strategy for futures markets with some help from Claude AI. Shoutout to everyone who gave me advice along the way—I really appreciate it! I’m sure there’s room for improvement, so feel free to share your thoughts… just go easy on me. :)

Trend Strategy + Impulse FilterThis is a Trend Strategy + Impulse Filter designed for trading in a dynamic market using both Simple Moving Average (SMA) and MACD indicators for trend and momentum analysis. The strategy includes risk management features like Stop Loss, Take Profit, and Trailing Stop to secure gains and limit losses. Additionally, it uses a Breakout Filter for confirmation, ensuring trades are taken only when the price breaks out from a specified range.

Key Features:

Trend Filter: Enter long when the price is above the SMA and MACD line crosses above the signal line. Enter short when the price is below the SMA and MACD line crosses below the signal line.

Breakout Filter: Only takes trades if the price breaks the previous high (for long) or low (for short) within a defined lookback period.

Risk Management: Set stop-loss and take-profit levels based on ATR for dynamic risk management.

Trailing Stop: Locks profits as the price moves in favor of the trade.

Position Sizing: Trade size is based on a percentage of the current equity.

Customizable Parameters: All indicators and risk management settings are adjustable to fit individual preferences.

This strategy is suitable for traders looking for a comprehensive approach that combines trend-following, momentum, and breakout filtering with solid risk management.

Ukrainian Description:

Це стратегія Trend + Impulse Filter, розроблена для торгівлі на динамічному ринку, використовуючи індикатори Простого ковзаючого середнього (SMA) та MACD для аналізу тренду та імпульсу. Стратегія включає в себе функції управління ризиками, такі як Stop Loss, Take Profit та Trailing Stop, щоб забезпечити прибутки та обмежити збитки. Крім того, вона використовує Breakout Filter для підтвердження, забезпечуючи виконання угод лише тоді, коли ціна пробиває визначений діапазон.

Основні характеристики:

Фільтр тренду: Вхід у лонг, коли ціна вище SMA, і MACD лінія перетинає сигнальну лінію знизу вгору. Вхід у шорт, коли ціна нижча за SMA, і MACD лінія перетинає сигнальну лінію зверху вниз.

Фільтр пробою: Торгові угоди відкриваються лише в разі пробою попереднього максимуму (для лонга) або мінімуму (для шорта) протягом заданого періоду.

Управління ризиками: Стоп-лосс та тейк-профіт визначаються на основі ATR для динамічного управління ризиками.

Trailing Stop: Фіксує прибутки, коли ціна рухається в бік угоди.

Розмір позиції: Розмір угоди залежить від відсотка від поточного балансу.

Налаштовувані параметри: Усі індикатори та налаштування управління ризиками можна відкоригувати відповідно до індивідуальних уподобань.

Ця стратегія підходить для трейдерів, які шукають комплексний підхід, що поєднує слідкування за трендом, імпульсом та фільтрацією пробоїв із надійним управлінням ризиками.

Scalping 15min: EMA + MACD + RSI + ATR-based SL/TP📈 Strategy: 15-Minute Scalping — EMA + MACD + RSI + ATR-based SL/TP

This scalping strategy is designed for 15-minute charts and combines trend-following and momentum confirmation with dynamic stop loss and take profit levels based on volatility.

🔧 Indicators Used:

EMA 50 — identifies the main trend

MACD Histogram — confirms momentum direction

RSI (14) — filters overbought/oversold conditions

ATR (14) — dynamically sets SL and TP based on market volatility

📊 Entry Conditions:

Long Entry:

Price is above EMA 50

MACD histogram is positive

RSI is above 50 but below 70

Short Entry:

Price is below EMA 50

MACD histogram is negative

RSI is below 50 but above 30

🛑 Risk Management:

Stop Loss: 1×ATR (user-configurable)

Take Profit: 2×ATR (user-configurable)

These values can be adjusted in the script inputs depending on your risk/reward preference or market conditions.

⚠️ Notes:

Strategy is optimized for scalping fast-moving pairs (e.g. crypto, forex).

Works best in trending markets.

Use backtesting and forward testing before live trading.

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :

- The script first calculates the ATR-based grid levels and ensures price action has sufficient volatility before allowing trades.

- An additional RSI filter is used to ensure trades are taken at ideal market conditions.

- Once a trade is executed, the script implements a trailing stop and predefined take profit to maximize gains while reducing risks.

---

Disclaimer :

Risk Warning :

This strategy is provided for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Users are advised to conduct their own due diligence and risk management before using this strategy in live trading.

The developer and publisher of this script are not responsible for any financial losses incurred by the use of this strategy. Market conditions, slippage, and execution quality can affect real-world trading outcomes.

Use this script at your own discretion and always trade responsibly.

ATM Option Selling StrategyATM Option Selling Strategy – Explained

This strategy is designed for intraday option selling based on the 9/15 EMA crossover, 50/80 MA trend filter, and RSI 50 level. It ensures that all trades are exited before market close (3:24 PM IST).

. Indicators Used:

9 EMA & 15 EMA → For short-term trend identification.

50 MA & 80 MA → To determine the overall trend.

RSI (14) → To confirm momentum (above or below 50 level).

2. Entry Conditions:

🔴 Sell ATM Call (CE) when:

Price is below 50 & 80 MA (Bearish trend).

9 EMA crosses below 15 EMA (Short-term trend turns bearish).

RSI is below 50 (Momentum confirms weakness).

🟢 Sell ATM Put (PE) when:

Price is above 50 & 80 MA (Bullish trend).

9 EMA crosses above 15 EMA (Short-term trend turns bullish).

RSI is above 50 (Momentum confirms strength).

3. Position Sizing & Risk Management:

Sell 375 quantity per trade (Lot size).

50-Point Stop Loss → If option premium moves against us by 50 points, exit.

50-Point Take Profit → If option premium moves in our favor by 50 points, book profit.

Exit all trades at 3:24 PM IST → No overnight positions.

4. Exit Conditions:

✅ Stop Loss or Take Profit Hits → Automatically exits based on a 50-point move.

✅ Time-Based Exit at 3:24 PM → Ensures no open positions at market close.

Why This Works?

✔ Trend Confirmation → 50/80 MA ensures we only sell options in the direction of the market trend.

✔ Momentum Confirmation → RSI prevents entering weak trades.

✔ Controlled Risk → SL and TP protect against large losses.

✔ No Overnight Risk → All trades close before market close.

Scalping Strategy Signal v2 by [INFINITYTRADER]Overview

This Pine Script (v6) implements a scalping strategy that uses higher timeframe data (default: 4H) to generate entry and exit signals, originally designed for the 15-minute timeframe with an option for 30-minute charts. The "Scalping Strategy Signal v2 by " integrates moving averages, RSI, volume, ATR, and candlestick patterns to identify trading opportunities. It features adjustable risk management with ATR-based stop-loss, take-profit, and trailing stops, plus dynamic position sizing based on user-set capital. Trades trigger only on the higher timeframe candle close (e.g., 4H) to limit activity within the same period. This closed-source script offers a structured scalping approach, blending multiple entry methods and risk controls for adaptability across market conditions.

What Makes It Unique

Unlike typical scalping scripts relying on single-indicator triggers (e.g., RSI alone or basic MA crossovers), this strategy combines four distinct entry methods—standard MA crossovers, RSI-based momentum shifts, trend-following shorts, and candlestick pattern logic—evaluated on a 4H timeframe for confirmation. This multi-layered design, paired with re-entry logic after losses and a mix of manual, ATR-based, and trailing exits, aims to balance trade frequency and reliability. The higher timeframe filter adds precision not commonly found in simpler scalping tools, while the 30-minute option enhances consistency by reducing noise.

How It Works

Timeframe Logic

Runs on a base timeframe (designed for 15-minute charts, with a 30-minute option) while pulling data from a user-chosen higher timeframe (default: 4H) for signal accuracy.

Limits entries to the close of each 4H candle, ensuring one trade per period to avoid over-trading in volatile conditions.

Indicators and Data

Moving Averages : Employs 21-period and 50-period simple moving averages on the higher timeframe to detect trends and signal entries/exits.

Volume : Requires volume to exceed 70% of its 20-period average on the higher timeframe for momentum confirmation.

RSI : Uses a 14-period RSI for overbought/oversold filtering and a 6-period RSI for precise entry timing.

ATR : Applies a 14-period Average True Range on the higher timeframe to set adaptive stop-loss and take-profit levels.

Candlestick Patterns : Analyzes consecutive green or red 4H bars for trend continuation signals.

Why These Indicators

The blend of moving averages, RSI, volume, ATR, and candlestick patterns forms a robust scalping framework. Moving averages establish trend context, RSI filters momentum and avoids extremes, volume confirms market activity, ATR adjusts risk to volatility, and candlestick patterns enhance entry timing with price action insights. Together, they target small, frequent moves in flat or trending markets, with the 4H filter reducing false signals common in lower-timeframe scalping.

Entry Conditions

Four entry methods are evaluated at the 4H candle close:

Standard Long Entry: Price crosses above the 21-period moving average, volume exceeds 70% of its 20-period average, and the 1H 14-period RSI is below 70—confirms uptrend momentum.

Special Long Entry: The 6-period RSI crosses above 23, price is more than 1.5 times the ATR from the 21-period moving average, and price exceeds its prior close—targets oversold bounces with a stop-loss at the 4H candle’s low.

Short Entries:

- RSI-Based: The 6-period RSI crosses below 68 with volume support—catches overbought pullbacks.

- Trend-Based: Price crosses below the 21-period moving average, volume is above 70% of its average, and the 1H 14-period RSI is above 30—confirms downtrends.

Red/Green Bar Logic: Two consecutive green 4H bars for longs or red 4H bars for shorts—uses candlestick patterns for continuation, with a tight stop-loss from the base timeframe candle.

Re-Entry Logic

Long : After a losing special long, triggers when the 6-period RSI crosses 27 and price crosses the 21-period moving average.

Short : After a losing short, triggers when the 6-period RSI crosses 50 and price crosses below the 21-period moving average.

Purpose: Offers recovery opportunities with stricter conditions.

Exit Conditions

Manual Exits: Longs close if the 21-period MA crosses below the 50-period MA or the 1H 14-period RSI exceeds 68; shorts close if the 21-period MA crosses above the 50-period MA or RSI drops below 25.

ATR-Based TP/SL: Stop-loss is entry price ± ATR × 1.5 (default); take-profit is ± ATR × 4 (default), checked at 4H close.

Trailing Stop: Adjusts ±6x ATR from peak/trough, closing if price retraces within 1x ATR.

Special/Tight SL: Special longs exit if price opens below the 4H candle’s low; 4th method entries use the base timeframe candle’s low/high, checked every bar.

Position Sizing

Bases trade value on user-set capital (default: 100 USDT), dividing by the higher timeframe close price for dynamic sizing.

Visualization

Displays a table at the bottom-right with current/previous signals, TP/SL levels, equity, trading pair, and trade size—color-coded for clarity (green for buy, red for sell).

Inputs

Initial Capital (USDT): Sets trade value (default: 100, min: 1).

ATR Stop-Loss Multiplier: Adjusts SL distance (default: 1.5, min: 1).

ATR Take-Profit Multiplier: Adjusts TP distance (default: 4, min: 1).

Higher Timeframe: Selects analysis timeframe (options: 1m, 5m, 15m, 30m, 1H, 4H, D, W; default: 4H).

Usage Notes

Intended Timeframe: Designed for 15-minute charts with 4H confirmation for precision and frequency; 30-minute charts improve consistency by reducing noise.

Backtesting: Adjust ATR multipliers and capital to match your asset’s volatility and risk tolerance.

Risk Management: Combines manual, ATR, and trailing exits—monitor to avoid overexposure.

Limitations: 4H candle-close dependency may delay entries in fast markets; RSI/volume filters can reduce trades in low-momentum periods.

Backtest Observations

Tested on BTC/USDT (4H higher timeframe, default settings: Initial Capital: 100 USDT, ATR SL: 1.5x, ATR TP: 4x) across market conditions, comparing 15-minute and 30-minute charts:

Bull Market (Jul 2023 - Dec 2023):

15-Minute: 277 long, 219 short; Win Rate: 42.74%; P&L: 108%; Drawdown: 1.99%; Profit Factor: 3.074.

30-Minute: 257 long, 215 short; Win Rate: 49.58%; P&L: 116.85%; Drawdown: 2.34%; Profit Factor: 3.14.

Notes: Moving average crossovers and green bar patterns suited this bullish phase; 30-minute improved win rate and P&L by filtering weaker signals.

Bear Market (Jan 2022 - Jun 2022):

15-Minute: 262 long, 211 short; Win Rate: 44.4%; P&L: 239.80%; Drawdown: 3.74%; Profit Factor: 3.419.

30-Minute: 250 long, 200 short; Win Rate: 52.22%; P&L: 258.77%; Drawdown: 5.34%; Profit Factor: 3.461.

Notes: Red bar patterns and RSI shorts thrived in the downtrend; 30-minute cut choppy reversals for better consistency.

Flat Market (Jan 2021 - Jun 2021):

15-Minute: 280 long, 208 short; Win Rate: 51.84%; P&L: 340.33%; Drawdown: 9.59%; Profit Factor: 2.924.

30-Minute: 270 long, 209 short; Win Rate: 55.11%; P&L: 315.42%; Drawdown: 7.21%; Profit Factor: 2.598.

Notes: High trade frequency and P&L showed strength in ranges; 30-minute lowered drawdown for better risk control.

Results reflect historical performance on BTC/USDT with default settings—users should test on their assets and timeframes. Past performance does not guarantee future results and is shared only to illustrate the strategy’s behavior.

Why It Works Well in Flat Markets

A "flat market" lacks strong directional trends, with price oscillating around moving averages, as in Jan 2021 - Jun 2021 for BTC/USDT. This strategy excels here because its crossover-based entries trigger frequently in tight ranges. In trending markets, an exit might not be followed by a new entry without a pullback, but flat markets produce multiple crossovers, enabling more trades. ATR-based TP/SL and trailing stops capture these small swings, while RSI and volume filters ensure momentum, driving high P&L and win rates.

Technical Details

Built in Pine Script v6 for TradingView compatibility.

Prevents overlapping trades with long/short checks.

Handles edge cases like zero division and auto-detects the trading pair’s base currency (e.g., BTC from BTCUSDT).

This strategy suits scalpers seeking structured entries and risk management. Test on 15-minute or 30-minute charts to match your style and market conditions.

RSI Pro+ (Bear market, financial crisis and so on EditionIn markets defined by volatility, fear, and uncertainty – the battlegrounds of bear markets and financial crises – you need tools forged in resilience. Introducing RSI Pro+, a strategy built upon a legendary indicator born in 1978, yet engineered with modern visual clarity to remain devastatingly effective even in the chaotic financial landscapes of 3078.

This isn't about complex algorithms predicting the unpredictable. It's about harnessing the raw, time-tested power of the Relative Strength Index (RSI) to identify potential exhaustion points and capitalize on oversold conditions. RSI Pro+ cuts through the noise, providing clear, actionable signals when markets might be poised for a relief bounce or reversal.

Core Technology (The 1978 Engine):

RSI Crossover Entry: The strategy initiates a LONG position when the RSI (default period 11) crosses above a user-defined low threshold (default 30). This classic technique aims to enter when selling pressure may be waning, offering potential entry points during sharp downturns or periods of consolidation after a fall.

Modern Enhancements (The 3078 Cockpit):

RSI Pro+ isn't just about the signal; it's about providing a professional-grade visual experience directly on your chart:

Entry Bar Highlight: A subtle background flash on the chart signals the exact bar where the RSI crossover condition is met, alerting you to potential entry opportunities.

Trade Bar Coloring: Once a trade is active, the price bars are subtly colored, giving you immediate visual confirmation that the strategy is live in the market.

Entry Price Line: A clear, persistent line marks your exact average entry price for the duration of the trade, serving as a crucial visual anchor.

Take Profit Line: Your calculated Take Profit target is plotted as a distinct line, keeping your objective clearly in sight.

Custom Entry Marker: A precise shape (▲) appears below the bar where the trade entry was actually executed, pinpointing the start of the position.

On-Chart Info Table (HUD): A clean, customizable Heads-Up Display appears when a trade is active, showing vital information at a glance:

Entry Price: Your position's average cost basis.

TP Target: The calculated price level for your Take Profit exit.

Current PnL%: Real-time Profit/Loss percentage for the open trade.

Full Customization: Nearly every aspect is configurable via the settings menu:

RSI Period & Crossover Level

Take Profit Percentage

Toggle ALL visual enhancements on/off individually

Position the Info Table wherever you prefer on the chart.

How to Use RSI Pro+:

Add to Chart: Apply the "RSI Pro+ (Bear market...)" strategy to your TradingView chart. Ensure any previous versions are removed.

Access Settings: Click the cogwheel icon (⚙️) next to the strategy name on your chart.

Configure Inputs (Crucial Step):

RSI Crossover Level: This is key. The default (30) targets standard oversold conditions. In severe downturns, you might experiment with lower levels (e.g., 25, 20) or higher ones (e.g., 40) depending on the asset and timeframe. Observe where RSI(11) typically bottoms out on your chart.

Take Profit Percentage (%): Define your desired profit target per trade (e.g., enter 0.5 for 0.5%, 1.0 for 1%). The default is a very small 0.11%.

RSI Period: While default is 11, you can adjust this (e.g., the standard 14).

Visual Enhancements: Enable or disable the visual features (background highlights, bar coloring, lines, markers, table) according to your preference using the checkboxes. Adjust table position.

Observe & Backtest: Watch how the strategy behaves on your chosen asset and timeframe. Use TradingView's Strategy Tester to analyze historical performance based on your settings. No strategy works perfectly everywhere; testing is essential.

Important Considerations:

Risk Management: This specific script version focuses on a Take Profit exit. It does not include an explicit Stop Loss. You MUST manage risk through appropriate position sizing, potentially adding a Stop Loss manually, or by modifying the script.

Oversold ≠ Reversal: An RSI crossover is an indicator of potential exhaustion, not a guarantee of a price reversal.

Fixed TP: A fixed percentage TP ensures small wins but may exit before larger potential moves.

Backtesting Limitations: Past performance does not guarantee future results.

RSI Pro+ strips away complexity to focus on a robust, time-honored principle, enhanced with modern visuals for the discerning trader navigating today's (and tomorrow's) challenging markets

Supertrend Fixed TP Unified with Time Filter (MSK)Trend Strategy Based on the SuperTrend Indicator

This strategy is based on the use of the adaptive SuperTrend indicator, which takes into account the current market volatility and acts as a dynamic trailing stop. The indicator is visualized on the chart with colors that change depending on the direction of the trade: green indicates an uptrend (long), while red indicates a downtrend (short).

How It Works:

A buy signal (long) is generated when a bar closes above the indicator line.

A sell signal (short) is triggered when a bar closes below the indicator line.

Strategy Settings:

Trading Modes :

Long only : Only long positions are allowed.

Short only : Only short positions are allowed.

Both : Both types of trades are permitted.

Take-Profit :

The strategy supports a simple percentage-based take-profit, allowing you to lock in profits during sharp price movements without waiting for a pullback.

The take-profit level and its value are visualized on the chart. Visualization can be disabled in the settings.

Colored Chart Areas :

Long and short areas on the chart are highlighted with background colors for easier analysis.

Price Level :

You can set a price level in the settings to restrict trade execution:

Long trades are executed only above the specified level.

Short trades are executed only below the specified level.

This mode can be enabled or disabled in the parameters.

________________________________________________________________

Описание стратегии (на русском языке)

Трендовая стратегия на основе индикатора SuperTrend

Стратегия основана на использовании адаптивного индикатора SuperTrend , который учитывает текущую волатильность рынка и играет роль динамического трейлинг-стопа. Индикатор визуализируется на графике цветом, который меняется в зависимости от направления сделки: зелёный цвет указывает на восходящий тренд (лонг), а красный — на нисходящий тренд (шорт).

Принцип работы:

Сигнал на покупку (лонг) генерируется при закрытии бара выше линии индикатора.

Сигнал на продажу (шорт) возникает при закрытии бара ниже линии индикатора.

Настройки стратегии:

Режимы торговли :

Long only : только лонговые позиции.

Short only : только шортовые позиции.

Both : разрешены оба типа сделок.

Тейк-профит :

Стратегия поддерживает простой процентный тейк-профит, что позволяет фиксировать прибыль при резком изменении цены без ожидания отката.

Уровень и значение тейк-профита визуализируются на графике. Визуализацию можно отключить в настройках.

Цветные области графика :

Лонговые и шортовые области графика выделяются цветом фона для удобства анализа.

Уровень цены :

В настройках можно задать уровень цены, который будет ограничивать выполнение сделок:

Лонговые сделки выполняются только выше указанного уровня.

Шортовые сделки выполняются только ниже указанного уровня.

Этот режим можно включать или отключать в параметрах.

Crypto Trend Reactor

Crypto Trend Reactor

🔧 By Rob Groff

Crypto Trend Reactor is a precision-engineered crypto trading strategy designed to identify high-quality trades through a fusion of advanced non-repainting indicators. This system integrates adaptive trend detection, volatility compression analysis, and directional momentum confirmation to provide clear, rule-based entries and dynamic trade management.

📜 Disclaimer

This script is for informational and educational purposes only. It is not financial advice or a recommendation to buy or sell any financial instrument. Always conduct your own research and consult with a professional advisor before making trading decisions.

✅ System Overview

This strategy is built around a synergy of robust, market-tested indicators that function together to filter noise, enhance trend clarity, and improve execution timing.

✅ McGinley Dynamic (Baseline)

An adaptive moving average that adjusts to price velocity, offering smoother and more responsive trend detection than traditional EMAs. Used to establish the primary trend direction.

✅ TTM Squeeze + Momentum

Detects volatility compression using Bollinger Bands inside Keltner Channels. When momentum aligns with a squeeze release, it signals explosive breakout potential — perfect for crypto markets.

✅ Vortex Indicator (Directional Volatility Filter)

Measures positive and negative trend strength. It confirms whether momentum aligns with trend direction, reducing false signals and choppy conditions.

✅ White Line (Bias Filter)

A simplified market structure average (High/Low midpoint) that acts as a bias filter. Aligning entries with this structural midpoint ensures trades are taken in the path of least resistance.

✅ Tether Line Cloud (Support/Resistance Mapping)

Fast and slow tether lines form a dynamic support/resistance cloud. This visual reference confirms price structure and trend shifts in real-time.

✅ ATR-Based Dynamic Stop Loss

Trailing stops adapt to volatility using ATR (with wick consideration). This enables better protection against random spikes while giving trades room to breathe.

✅ Fixed Multi-Level Take Profits (TP1 & TP2)

Position-reducing take profit levels help secure gains while maintaining trade flexibility. After TP2 is hit, the strategy supports dynamic re-entry if the trend resumes.

✅ Advanced Features

✅ Fully non-repainting logic

✅ Dynamic re-entry support after TP2 or stop-out

✅ Separate take profit and stop loss logic for long and short trades

✅ Visual trade dashboard with live PnL, win rate, position info, and trend status

✅ TTM Squeeze dots shown as ✅ blue dots below/above bars

✅ Bar coloring and cloud fills based on real-time trend alignment

✅ Built-in date filter for backtest range control

✅ Recommended Use

Timeframe: Best optimized for the 1-hour chart, but effective on other timeframes with minor tuning

Market: Designed for crypto, but also functional in other volatile asset classes

Strategy Mode: Works best in trending environments. Avoids ranging conditions via Vortex filtering and multi-confirmation layers

✅ Best Practices

✅ Confirm entries only when all filters align (trend, bias, volatility, and momentum)

✅ Monitor the dashboard for live trade metrics and trend health

✅ Use the built-in stop and TP logic to automate exits

✅ Backtest with various parameter settings to fine-tune for specific coins or volatility profiles

This script represents the fusion of structure, momentum, trend, and volatility — delivering an edge-driven approach for serious crypto traders seeking consistent execution and high-probability setups.

DrNon Action Zone📈 Strategy Title:

DrNon Action Zone — EMA Cross with ATR Stop, % Take-Profit, Alerts & Date Range

⸻

🧠 Strategy Concept:

DrNon Action Zone is a long-only trend-following strategy that enters trades when momentum aligns with long-term trend confirmation. It uses:

• EMA Cross (Fast vs. Slow) to identify momentum shift

• Optional EMA Filter based on days to confirm that price is in a “trend zone”

• ATR-based trailing stop for adaptive risk management

• Percentage Take-Profit for reward targeting

• Date Range Filter for focused backtesting or event-based execution

It also includes alerts, visual signals, and full customization via inputs.

⸻

⚙️ Strategy Inputs Explained:

Input Name Description

Fast EMA Length Period of the short-term EMA used for crossover signals (default: 5)

Slow EMA Length Period of the long-term EMA used for crossover signals (default: 200)

ATR Period Period used to calculate the Average True Range (ATR)

ATR Multiplier Multiplies ATR value to calculate the trailing stop distance

Take-Profit % Percentage above entry price to exit the trade for profit

Use EMA Filter? If enabled, long entries require price to be above a customizable EMA filter

EMA Filter Days Number of days used for EMA filter (converted to bars based on chart timeframe)

Use Date Range? Enable or disable the date filter

Start Date / End Date Specify a custom range to apply the strategy

⸻

✅ Long Entry Conditions (The Action Zone):

A long trade is entered when:

1. EMA(Fast) crosses above EMA(Slow)

2. If EMA Filter is enabled, Close > EMA(Filter Days)

3. If Date Filter is enabled, current candle is within specified start and end dates

⸻

❌ Exit Conditions:

The strategy will close the position when either:

• Price drops to ATR-based trailing stop, OR

• Price reaches the Take-Profit % target

⸻

🛎️ Alerts:

Alert Name Trigger Condition

Long Entry Alert EMA cross and all filters passed (entry signal triggered)

Exit Alert Price hit ATR Stop or Take-Profit (exit signal triggered)

⸻

📊 Visual Elements:

• Yellow Line — Fast EMA

• Blue Line — Slow EMA

• Purple Line — EMA Filter (based on user-defined days)

• Red Line — ATR-based Trailing Stop

• Lime Line — Take-Profit Level

• Green Triangle — Long Entry Signal (on crossover)

⸻

🧪 Backtesting Tips:

• Adjust EMA Filter Days to simulate different trend conditions (e.g., 100d, 150d, 200d).

• Use ATR Multiplier to adapt the stop-loss to market volatility.

• Combine date filtering with known events (e.g., earnings, FOMC meetings).

• Test in multiple timeframes — 1H, 4H, or Daily for stronger signals.

Crypto Strategy SUSDT 10 minThis strategy is designed to trade the **SUSDT** pair on a **10-minute time frame**, using a combination of an Exponential Moving Average (EMA) and percentage-based Stop Loss (SL) and Take Profit (TP) levels.

### How the strategy works:

1. **EMA Calculation**:

- The strategy calculates a 24-period Exponential Moving Average (EMA) based on the closing price.

- This EMA serves as the primary trend indicator.

2. **Entry Conditions**:

- **Long Position**: A long position is entered when the closing price is above the EMA and the opening price is below the EMA. This indicates a potential upward trend.

- **Short Position**: A short position is entered when the closing price is below the EMA and the opening price is above the EMA. This indicates a potential downward trend.

3. **Stop Loss and Take Profit**:

- Both Stop Loss (SL) and Take Profit (TP) are calculated based on the entry price of the position.

- **For Long Positions**:

- Stop Loss is set as a percentage below the entry price.

- Take Profit is set as a percentage above the entry price.

- **For Short Positions**:

- Stop Loss is set as a percentage above the entry price.

- Take Profit is set as a percentage below the entry price.

- The percentage values for SL and TP can be adjusted in the strategy's settings (default: SL = 2%, TP = 4%).

4. **Exit Conditions**:

- The position is closed automatically when either the Stop Loss or Take Profit level is reached.

5. **Visualization**:

- The 24-period EMA is plotted on the chart as a blue line, helping visualize the trend direction.

### Key Features:

- **Pair and Time Frame**: The strategy is optimized for the SUSDT pair on a 10-minute time frame.

- **Customizable Parameters**: Users can adjust the Stop Loss and Take Profit percentages to suit their risk tolerance and trading style.

- **Trend-Following Approach**: The strategy uses the EMA to identify and follow the current market trend.

This strategy is simple yet effective for capturing trends while managing risk through predefined Stop Loss and Take Profit levels.

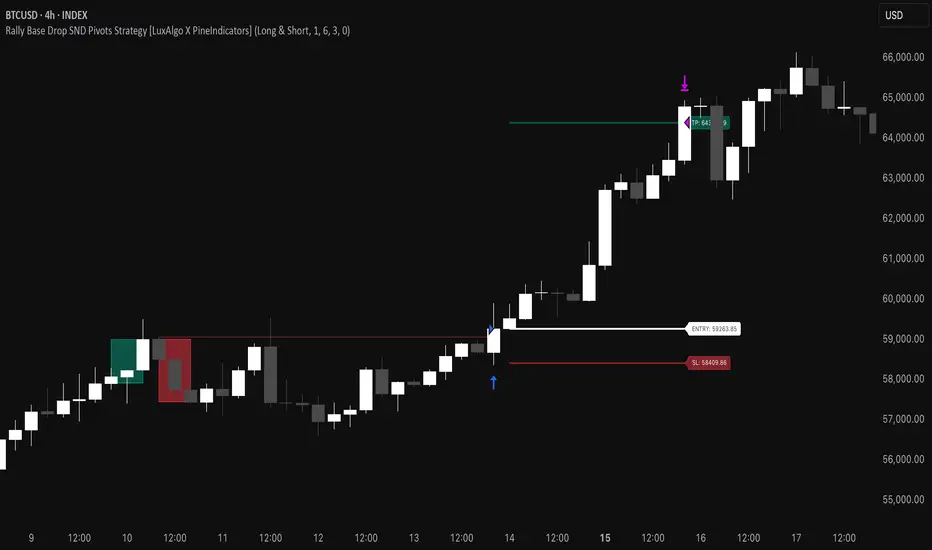

Rally Base Drop SND Pivots Strategy [LuxAlgo X PineIndicators]This strategy is based on the Rally Base Drop (RBD) SND Pivots indicator developed by LuxAlgo. Full credit for the concept and original indicator goes to LuxAlgo.

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand trading system that detects pivot points based on Rally, Base, and Drop (RBD) candles. This strategy automatically identifies key market structure levels, allowing traders to:

Identify pivot-based supply and demand (SND) zones.

Use fixed criteria for trend continuation or reversals.

Filter out market noise by requiring structured price formations.

Enter trades based on breakouts of key SND pivot levels.

How the Rally Base Drop SND Pivots Strategy Works

1. Pivot Point Detection Using RBD Candles

The strategy follows a rigid market structure methodology, where pivots are detected only when:

A Rally (R) consists of multiple consecutive bullish candles.

A Drop (D) consists of multiple consecutive bearish candles.

A Base (B) is identified as a transition between Rallies and Drops, acting as a pivot point.

The pivot level is confirmed when the formation is complete.

Unlike traditional fractal-based pivots, RBD Pivots enforce stricter structural rules, ensuring that each pivot:

Has a well-defined bullish or bearish price movement.

Reduces false signals caused by single-bar fluctuations.

Provides clear supply and demand levels based on structured price movements.

These pivot levels are drawn on the chart using color-coded boxes:

Green zones represent bullish pivot levels (Rally Base formations).

Red zones represent bearish pivot levels (Drop Base formations).

Once a pivot is confirmed, the high or low of the base candle is used as the reference level for future trades.

2. Trade Entry Conditions

The strategy allows traders to select from three trading modes:

Long Only – Only takes long trades when bullish pivot breakouts occur.

Short Only – Only takes short trades when bearish pivot breakouts occur.

Long & Short – Trades in both directions based on pivot breakouts.

Trade entry signals are triggered when price breaks through a confirmed pivot level:

Long Entry:

A bullish pivot level is formed.

Price breaks above the bullish pivot level.

The strategy enters a long position.

Short Entry:

A bearish pivot level is formed.

Price breaks below the bearish pivot level.

The strategy enters a short position.

The strategy includes an optional mode to reverse long and short conditions, allowing traders to experiment with contrarian entries.

3. Exit Conditions Using ATR-Based Risk Management

This strategy uses the Average True Range (ATR) to calculate dynamic stop-loss and take-profit levels:

Stop-Loss (SL): Placed 1 ATR below entry for long trades and 1 ATR above entry for short trades.

Take-Profit (TP): Set using a Risk-Reward Ratio (RR) multiplier (default = 6x ATR).

When a trade is opened:

The entry price is recorded.

ATR is calculated at the time of entry to determine stop-loss and take-profit levels.

Trades exit automatically when either SL or TP is reached.

If reverse conditions mode is enabled, stop-loss and take-profit placements are flipped.

Visualization & Dynamic Support/Resistance Levels

1. Pivot Boxes for Market Structure

Each pivot is marked with a colored box:

Green boxes indicate bullish demand zones.

Red boxes indicate bearish supply zones.

These boxes remain on the chart to act as dynamic support and resistance levels, helping traders identify key price reaction zones.

2. Horizontal Entry, Stop-Loss, and Take-Profit Lines

When a trade is active, the strategy plots:

White line → Entry price.

Red line → Stop-loss level.

Green line → Take-profit level.

Labels display the exact entry, SL, and TP values, updating dynamically as price moves.

Customization Options

This strategy offers multiple adjustable settings to optimize performance for different market conditions:

Trade Mode Selection → Choose between Long Only, Short Only, or Long & Short.

Pivot Length → Defines the number of required Rally & Drop candles for a pivot.

ATR Exit Multiplier → Adjusts stop-loss distance based on ATR.

Risk-Reward Ratio (RR) → Modifies take-profit level relative to risk.

Historical Lookback → Limits how far back pivot zones are displayed.

Color Settings → Customize pivot box colors for bullish and bearish setups.

Considerations & Limitations

Pivot Breakouts Do Not Guarantee Reversals. Some pivot breaks may lead to continuation moves instead of trend reversals.

Not Optimized for Low Volatility Conditions. This strategy works best in trending markets with strong momentum.

ATR-Based Stop-Loss & Take-Profit May Require Optimization. Different assets may require different ATR multipliers and RR settings.

Market Noise May Still Influence Pivots. While this method filters some noise, fake breakouts can still occur.

Conclusion

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand system that combines:

Pivot-based market structure analysis (using Rally, Base, and Drop candles).

Breakout-based trade entries at confirmed SND levels.

ATR-based dynamic risk management for stop-loss and take-profit calculation.

This strategy helps traders:

Identify high-probability supply and demand levels.

Trade based on structured market pivots.

Use a systematic approach to price action analysis.

Automatically manage risk with ATR-based exits.

The strict pivot detection rules and built-in breakout validation make this strategy ideal for traders looking to:

Trade based on market structure.

Use defined support & resistance levels.

Reduce noise compared to traditional fractals.

Implement a structured supply & demand trading model.

This strategy is fully customizable, allowing traders to adjust parameters to fit their market and trading style.

Full credit for the original concept and indicator goes to LuxAlgo.

Gradient Trend Filter STRATEGY [ChartPrime/PineIndicators]This strategy is based on the Gradient Trend Filter indicator developed by ChartPrime. Full credit for the concept and indicator goes to ChartPrime.

The Gradient Trend Filter Strategy is designed to execute trades based on the trend analysis and filtering system provided by the Gradient Trend Filter indicator. It integrates a noise-filtered trend detection system with a color-gradient visualization, helping traders identify trend strength, momentum shifts, and potential reversals.

How the Gradient Trend Filter Strategy Works

1. Noise Filtering for Smoother Trends

To reduce false signals caused by market noise, the strategy applies a three-stage smoothing function to the source price. This function ensures that trend shifts are detected more accurately, minimizing unnecessary trade entries and exits.

The filter is based on an Exponential Moving Average (EMA)-style smoothing technique.

It processes price data in three successive passes, refining the trend signal before generating trade entries.

This filtering technique helps eliminate minor fluctuations and highlights the true underlying trend.

2. Multi-Layered Trend Bands & Color-Based Trend Visualization

The Gradient Trend Filter constructs multiple trend bands around the filtered trend line, acting as dynamic support and resistance zones.

The mid-line changes color based on the trend direction:

Green for uptrends

Red for downtrends

A gradient cloud is formed around the trend line, dynamically shifting colors to provide early warning signals of trend reversals.

The outer bands function as potential support and resistance, helping traders determine stop-loss and take-profit zones.

Visualization elements used in this strategy:

Trend Filter Line → Changes color between green (bullish) and red (bearish).

Trend Cloud → Dynamically adjusts color based on trend strength.

Orange Markers → Appear when a trend shift is confirmed.

Trade Entry & Exit Conditions

This strategy automatically enters trades based on confirmed trend shifts detected by the Gradient Trend Filter.

1. Trade Entry Rules

Long Entry:

A bullish trend shift is detected (trend direction changes to green).

The filtered trend value crosses above zero, confirming upward momentum.

The strategy enters a long position.

Short Entry:

A bearish trend shift is detected (trend direction changes to red).

The filtered trend value crosses below zero, confirming downward momentum.

The strategy enters a short position.

2. Trade Exit Rules

Closing a Long Position:

If a bearish trend shift occurs, the strategy closes the long position.

Closing a Short Position:

If a bullish trend shift occurs, the strategy closes the short position.

The trend shift markers (orange diamonds) act as a confirmation signal, reinforcing the validity of trade entries and exits.

Customization Options

This strategy allows traders to adjust key parameters for flexibility in different market conditions:

Trade Direction: Choose between Long Only, Short Only, or Long & Short .

Trend Length: Modify the length of the smoothing function to adapt to different timeframes.

Line Width & Colors: Customize the visual appearance of trend lines and cloud colors.

Performance Table: Enable or disable the equity performance table that tracks historical trade results.

Performance Tracking & Reporting

A built-in performance table is included to monitor monthly and yearly trading performance.

The table calculates monthly percentage returns, displaying them in a structured format.

Color-coded values highlight profitable months (blue) and losing months (red).

Tracks yearly cumulative performance to assess long-term strategy effectiveness.

Traders can use this feature to evaluate historical performance trends and optimize their strategy settings accordingly.

How to Use This Strategy

Identify Trend Strength & Reversals:

Use the trend line and cloud color changes to assess trend strength and detect potential reversals.

Monitor Momentum Shifts:

Pay attention to gradient cloud color shifts, as they often appear before the trend line changes color.

This can indicate early momentum weakening or strengthening.

Act on Trend Shift Markers:

Use orange diamonds as confirmation signals for trend shifts and trade entry/exit points.

Utilize Cloud Bands as Support/Resistance:

The outer bands of the cloud serve as dynamic support and resistance, helping with stop-loss and take-profit placement.

Considerations & Limitations

Trend Lag: Since the strategy applies a smoothing function, entries may be slightly delayed compared to raw price action.

Volatile Market Conditions: In high-volatility markets, trend shifts may occur more frequently, leading to higher trade frequency.

Optimized for Trend Trading: This strategy is best suited for trending markets and may produce false signals in sideways (ranging) conditions.

Conclusion

The Gradient Trend Filter Strategy is a trend-following system based on the Gradient Trend Filter indicator by ChartPrime. It integrates noise filtering, trend visualization, and gradient-based color shifts to help traders identify strong market trends and potential reversals.

By combining trend filtering with a multi-layered cloud system, the strategy provides clear trade signals while minimizing noise. Traders can use this strategy for long-term trend trading, momentum shifts, and support/resistance-based decision-making.

This strategy is a fully automated system that allows traders to execute long, short, or both directions, with customizable settings to adapt to different market conditions.

Credit for the original concept and indicator goes to ChartPrime.

is_strategyCorrection-Adaptive Trend Strategy (Open-Source)

Core Advantage: Designed specifically for the is_correction indicator, with full transparency and customization options.

Key Features:

Open-Source Code:

✅ Full access to the strategy logic – study how every trade signal is generated.

✅ Freedom to customize – modify entry/exit rules, risk parameters, or add new indicators.

✅ No black boxes – understand and trust every decision the strategy makes.

Built for is_correction:

Filters out false signals during market noise.

Works only in confirmed trends (is_correction = false).

Adaptable for Your Needs:

Change Take Profit/Stop Loss ratios directly in the code.

Add alerts, notifications, or integrate with other tools (e.g., Volume Profile).

For Developers/Traders:

Use the code as a template for your own strategies.

Test modifications risk-free on historical data.

How the Strategy Works:

Main Goal:

Automatically buys when the price starts rising and sells when it starts falling, but only during confirmed trends (ignoring temporary pullbacks).

What You See on the Chart:

📈 Up arrows ▼ (below the candle) = Buy signal.

📉 Down arrows ▲ (above the candle) = Sell signal.

Gray background = Market is in a correction (no trades).

Key Mechanics:

Buy Condition:

Price closes higher than the previous candle + is_correction confirms the main trend (not a pullback).

Example: Red candle → green candle → ▼ arrow → buy.

Sell Condition:

Price closes lower than the previous candle + is_correction confirms the trend (optional: turn off short-selling in settings).

Exit Rules:

Closes trades automatically at:

+0.5% profit (adjustable in settings).

-0.5% loss (adjustable).

Or if a reverse signal appears (e.g., sell signal after a buy).

User-Friendly Settings:

Sell – On (default: ON):

ON → Allows short-selling (selling when price falls).

OFF → Strategy only buys and closes positions.

Revers (default: OFF):

ON → Inverts signals (▼ = sell, ▲ = buy).

%Profit & %Loss:

Adjust these values (0-30%) to increase/decrease profit targets and risk.

Example Scenario:

Buy Signal:

Price rises for 3 days → green ▼ arrow → strategy buys.

Stop loss set 0.5% below entry price.

If price keeps rising → trade closes at +0.5% profit.

Correction Phase:

After a rally, price drops for 1 day → gray background → strategy ignores the drop (no action).

Stop Loss Trigger:

If price drops 0.5% from entry → trade closes automatically.

Key Features:

Correction Filter (is_correction):

Acts as a “noise filter” → avoids trades during temporary pullbacks.

Flexibility:

Disable short-selling, flip signals, or tweak profit/loss levels in seconds.

Transparency:

Open-source code → see exactly how every signal is generated (click “Source” in TradingView).

Tips for Beginners:

Test First:

Run the strategy on historical data (click the “Chart” icon in TradingView).

See how it performed in the past.

Customize It:

Increase %Profit to 2-3% for volatile assets like crypto.

Turn off Sell – On if short-selling confuses you.

Trust the Stop Loss:

Even if you think the price will rebound, the strategy will close at -0.5% to protect your capital.

Where to Find Settings:

Click the strategy name on the top-left of your chart → adjust sliders/toggles in the menu.

Русская Версия

Трендовая стратегия с открытым кодом

Главное преимущество: Полная прозрачность логики и адаптация под ваши нужды.

Особенности:

Открытый исходный код:

✅ Видите всю «кухню» стратегии – как формируются сигналы, когда открываются сделки.

✅ Меняйте правила – корректируйте тейк-профит, стоп-лосс или добавляйте новые условия.

✅ Никаких секретов – вы контролируете каждое правило.

Заточка под is_correction:

Игнорирует ложные сигналы в коррекциях.

Работает только в сильных трендах (is_correction = false).

Гибкая настройка:

Подстройте параметры под свой риск-менеджмент.

Добавьте свои индикаторы или условия для входа.

Для трейдеров и разработчиков:

Используйте код как основу для своих стратегий.

Тестируйте изменения на истории перед реальной торговлей.

Простыми словами:

Почему это удобно:

Открытый код = полный контроль. Вы можете:

Увидеть, как именно стратегия решает купить или продать.

Изменить правила закрытия сделок (например, поставить TP=2% вместо 1.5%).

Добавить новые условия (например, торговать только при высоком объёме).

Примеры кастомизации:

Новички: Меняйте только TP/SL в настройках (без кодинга).

Продвинутые: Добавьте RSI-фильтр, чтобы избегать перекупленности.

Разработчики: Встройте стратегию в свою торговую систему.

Как начать:

Скачайте код из TradingView.

Изучите логику в разделе strategy.entry/exit.

Меняйте параметры в блоке input.* (безопасно!).

Тестируйте изменения и оптимизируйте под свои цели.

Как работает стратегия:

Главная задача:

Автоматически покупает, когда цена начинает расти, и продаёт, когда падает. Но делает это «умно» — только когда рынок в основном тренде, а не во временном откате (коррекции).

Что видно на графике:

📈 Стрелки вверх ▼ (под свечой) — сигнал на покупку.

📉 Стрелки вниз ▲ (над свечой) — сигнал на продажу.

Серый фон — рынок в коррекции (не торгуем).

Как это работает:

Когда покупаем:

Если цена закрылась выше предыдущей и индикатор is_correction показывает «основной тренд» (не коррекция).

Пример: Была красная свеча → стала зелёная → появилась стрелка ▼ → покупаем.

Когда продаём:

Если цена закрылась ниже предыдущей и is_correction подтверждает тренд (опционально, можно отключить в настройках).

Когда закрываем сделку:

Автоматически при достижении:

+0.5% прибыли (можно изменить в настройках).

-0.5% убытка (можно изменить).

Или если появился противоположный сигнал (например, после покупки пришла стрелка продажи).

Настройки для чайников:

«Sell – On» (включено по умолчанию):

Если включено → стратегия будет продавать в шорт.

Если выключено → только покупки и закрытие позиций.

«Revers» (выключено по умолчанию):

Если включить → стратегия будет работать наоборот (стрелки ▼ = продажа, ▲ = покупка).

«%Profit» и «%Loss»:

Меняйте эти цифры (от 0 до 30), чтобы увеличить/уменьшить прибыль и риски.

Пример работы:

Сигнал на покупку:

Цена 3 дня растет → появляется зелёная стрелка ▼ → стратегия покупает.

Стоп-лосс ставится на 0.5% ниже цены входа.

Если цена продолжает расти → сделка закрывается при +0.5% прибыли.

Коррекция:

После роста цена падает на 1 день → фон становится серым → стратегия игнорирует это падение (не закрывает сделку).

Стоп-лосс:

Если цена упала на 0.5% от точки входа → сделка закрывается автоматически.

Важные особенности:

Фильтр коррекций (is_correction):

Это «защита от шума» — стратегия не реагирует на мелкие откаты, работая только в сильных трендах.

Гибкие настройки:

Можно запретить шорты, перевернуть сигналы или изменить уровни прибыли/убытка за 2 клика.

Прозрачность:

Весь код открыт → вы можете увидеть, как формируется каждый сигнал (меню «Исходник» в TradingView).

Советы для новичков:

Начните с теста:

Запустите стратегию на исторических данных (кнопка «Свеча» в окне TradingView).

Посмотрите, как она работала в прошлом.

Настройте под себя:

Увеличьте %Profit до 2-3%, если торгуете валюты.

Отключите «Sell – On», если не понимаете шорты.

Доверяйте стоп-лоссу:

Даже если кажется, что цена развернётся — стратегия закроет сделку при -0.5%, защитив ваш депозит.

Где найти настройки:

Кликните на название стратегии в верхнем левом углу графика → откроется меню с ползунками и переключателями.

Важно: Стратегия предоставляет «рыбу» – чтобы она стала «уловистой», адаптируйте её под свой стиль торговли!

Color Code Overlay StrategyColor Code Overlay Strategy

This strategy utilizes a custom color-coded overlay to provide accurate buy and sell signals based on dynamic color changes of the candles. The indicator works by calculating a color shift between bullish (green) and bearish (red) candles, with the color change logic driven by both price movement and volatility.

How the Color Change is Calculated:

The color change is determined by comparing the closing price relative to the opening price of each candle, as is typical with a traditional bullish or bearish candle. However, to make this strategy more adaptive to market conditions, the color change is further refined by incorporating the Average True Range (ATR).

Volatility Adjusted Color Shift: The strategy calculates a dynamic threshold based on the ATR value, which represents market volatility. If the price movement between the open and close of the candle exceeds a specific percentage of the ATR, the color of the candle shifts from red (bearish) to green (bullish) or vice versa.

Threshold Calculation: A fixed percentage (e.g., 1%) of the ATR range is used to define the minimum price movement required for a color change. This ensures that only significant price movements, adjusted for volatility, trigger the color shift. The larger the ATR (higher volatility), the greater the price movement required to cause a change in color.

Bullish to Bearish (Green to Red): When the candle closes lower than the open, and the price movement exceeds the dynamic threshold based on ATR, the candle color changes from green to red, signaling a potential bearish reversal.

Bearish to Bullish (Red to Green): When the candle closes higher than the open, and the price movement exceeds the ATR-based threshold, the candle color shifts from red to green, signaling a potential bullish reversal.

Key Features: